-

The most loved way to get paid as you work1No hard or soft credit check

The most loved way to get paid as you work1No hard or soft credit check -

![image of a user walking happily]()

-

![image of a user carrying their kids while using EarnIn web application on a laptop]()

-

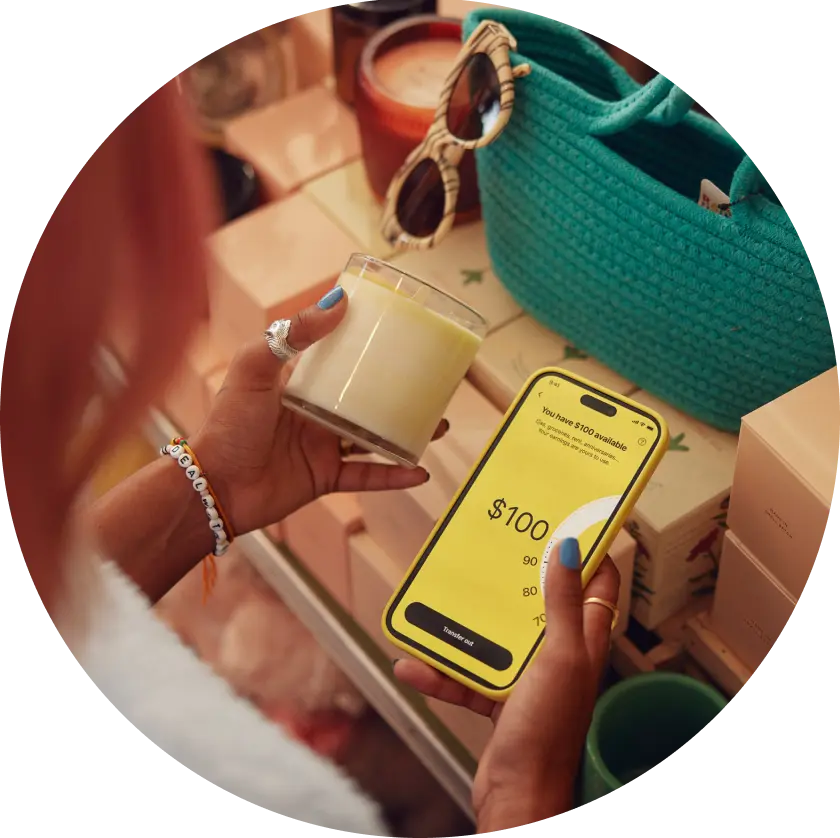

![image of a user opening EarnIn application on a mobile phone while considering to buy an item]()

-

![image of a person smiling to another person]()

EarnIn is a financial technology company, not a bank. Bank products are issued by Evolve Bank & Trust, Member FDIC. The EarnIn Card is issued pursuant to a license from Visa USA Inc.

1Subject to your available earnings, Daily Max and Pay Period Max. Restrictions and/or third party fees may apply, see EarnIn.com/TOS for details

2Fees apply to use Lightning Speed. Lightning Speed may not be available to all Community Members. Transfers may take up to thirty minutes, actual transfer speeds will depend on your bank. Restrictions and/or third party fees may apply, see Cash Out User Agreement for details

3Calculated on the VantageScore 3.0 model. Your VantageScore 3.0 from Experian® indicates your credit risk level and is not used by all lenders, so don't be surprised if your lender uses a score that's different from your VantageScore 3.0. Learn more: https://www.experian.com/assets/consumer-information/product-sheets/vantagescore-3.pdf

4Balance Shield cash out is subject to your available earnings, Daily Max and Pay Period Max. Other restrictions and/or third-party fees may apply. For more information visit EarnIn.com/TOS

5Tip Yourself Account funds are held with Evolve Bank & Trust, member FDIC and FDIC insured up to $250,000. Tip Yourself is a 0% Annual Percentage Yield and $0 monthly fee service. Your Tip Yourself Account and any Tip Jars are not Savings Accounts. For more information/details visit https://www.earnin.com/evolve-bank-and-trust

6EarnIn does not charge hidden fees for use of its services. EarnIn does not charge interest on Cash Outs. Restrictions and/or third party fees may apply, see EarnIn.com/TOS for details